Movement duo helps single mom move home

It had been a difficult two years for Teresa Barnette, a recent divorcee, when she had a tearful phone conversation with a Movement Mortgage loan officer.

After 20 years together, Teresa and her husband had separated, leaving the single mother and her youngest daughter sleeping on a friend's pullout sofa for nearly a year. After a second year of renting an apartment, Teresa dared to dream that her monthly rent might be better spent going towards a small home in her native Upstate South Carolina.

The story struck a chord with loan officer Shawneke Wilson (NMLS #1575907), who recalled her own mother starting over with three children after a divorce.

“My initial call with Teresa was very emotional,” Shawneke says. “I left my desk and went to the prayer room as she shared her story with me. I encouraged her and read a few things that were scripture-based. I let her know we would walk this process together.”

The bond between the two women, and a partnership between two Movement Mortgage loan officers, helped Teresa find a new beginning for herself and her daughter.

Passing the first hurdle

Despite a challenging few years, Teresa was a solid candidate for a home loan. She had long-term employment with a large financial institution and supplemented that income working as a restaurant server. Over the previous 24 months, she had diligently paid down her credit card debt. That, and her good credit score, helped her qualify for home loan pre-approval — as long as they could arrange for down payment assistance.

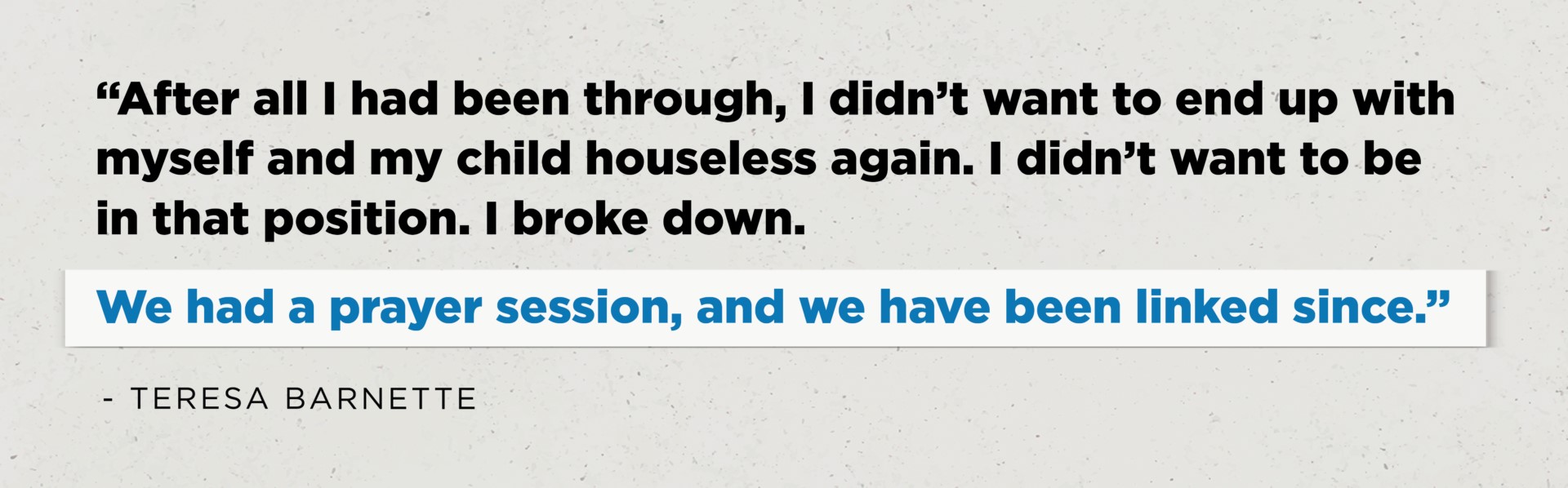

When she was approved, Shawneke called Teresa to give her the good news. Teresa's response was more muted than Shawneke expected. “I was happy, but I was nervous,” remembers Teresa. “After all we'd been through, I didn't want my daughter and I to end up house-less again. I didn't want to be in that position. I broke down.”

So Shawneke and Teresa had a prayer session. “And we have been linked since,” Teresa says.

Ready for what's next

With loan pre-approval and qualification for down payment assistance, Teresa had passed the first hurdle. But with home sales inventory at record lows, finding the right home that qualified for the assistance programs was the next challenge.

As the search for a house intensified, Shawneke thought Teresa might find one that qualified for a loan backed by the U.S. Department of Agriculture. One of the least-known mortgage assistance programs, a USDA loan allows middle-class homebuyers to purchase eligible rural and suburban homes without a down payment. For Teresa, such a loan would make it possible for her to become a homeowner without depleting her personal savings.

Despite their search, Teresa and her Realtor struggled to find a home that qualified for the USDA loan. Shawneke suggested they connect with Ed Butler (NMLS #108407), a Movement Mortgage retail loan officer familiar with South Carolina's forgivable down payment assistance program.

Tapping into experience

“People considering first homes do not always realize that programs are available to assist with the down payment hurdle,” Ed says. He should know: At Movement, Ed completes home financing for a half-dozen USDA-approved loans each month.

“Typically, first-time homeowners do not have the down payment,” he explains. “There are people out there who can afford the $1,200 mortgage, but they can't come up with 7% down and up to $5,000 in closing costs.”

Talking about those specific financial hurdles is one of the first conversations Movement Mortgage loan officers have with potential homebuyers. Even before a potential homebuyer finds a possible dream house, a Movement Mortgage loan officer will see what programs a buyer might qualify for and how such a program could ease the path to becoming a homeowner.

“Everyone has a desired monthly payment in mind, but there are many factors, including the borrower's credit score, car payments and student loans,” Ed explains. “There are a lot of variables and we look at the whole picture.”

“That's the benefit of being more of an advisor to home buyers than just doing a transaction for them,” Ed says. “We tried to find the best product for Teresa.”

Going the last mile

Ultimately, Teresa fell in love with a three-bedroom home that qualified for the USDA program with a 30-year term. Ed and Shawneke teamed up to shepherd the deal to closing. Because of Ed's relationship with the Realtor assisting Teresa, they negotiated for the seller to pay closing costs of nearly $4,500.

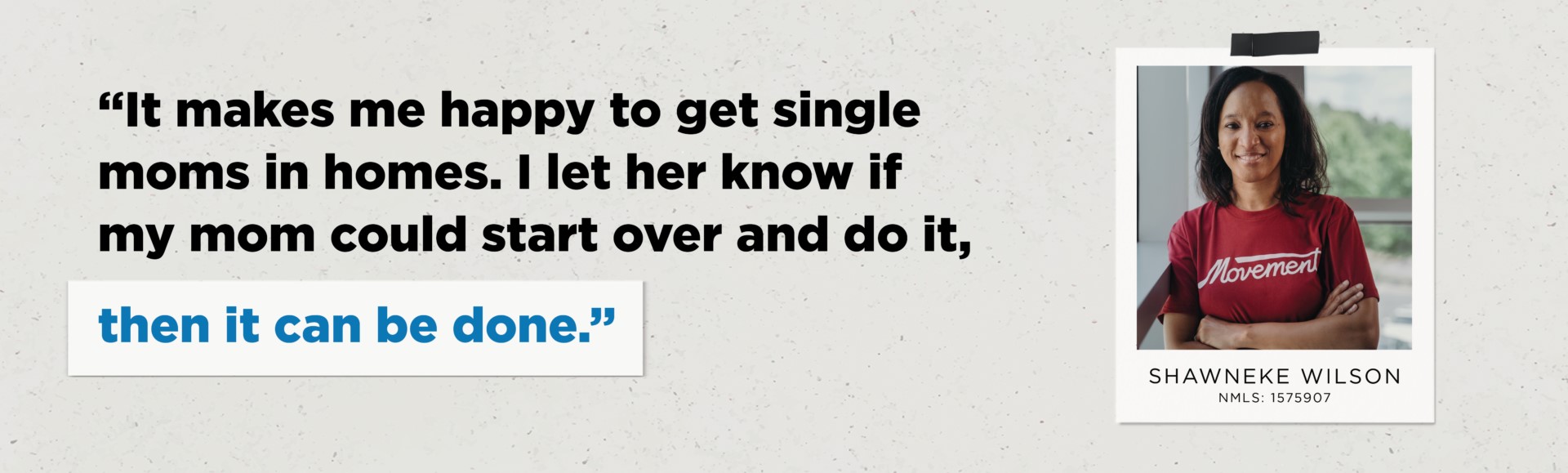

And as Ed worked with Teresa to secure a mortgage for her chosen home, Shawneke remained behind the scenes, sending encouragement and helping where needed. “It makes me happy to get single moms in homes,” she says. “I let her know if my mom could start over and do it, then you know it can be done.”

Having to bring no additional cash to the closing and receiving her earnest money back helped ensure Teresa was on solid footing as a new homeowner. She closed on the new home in May with an attractive 3.15% interest rate.

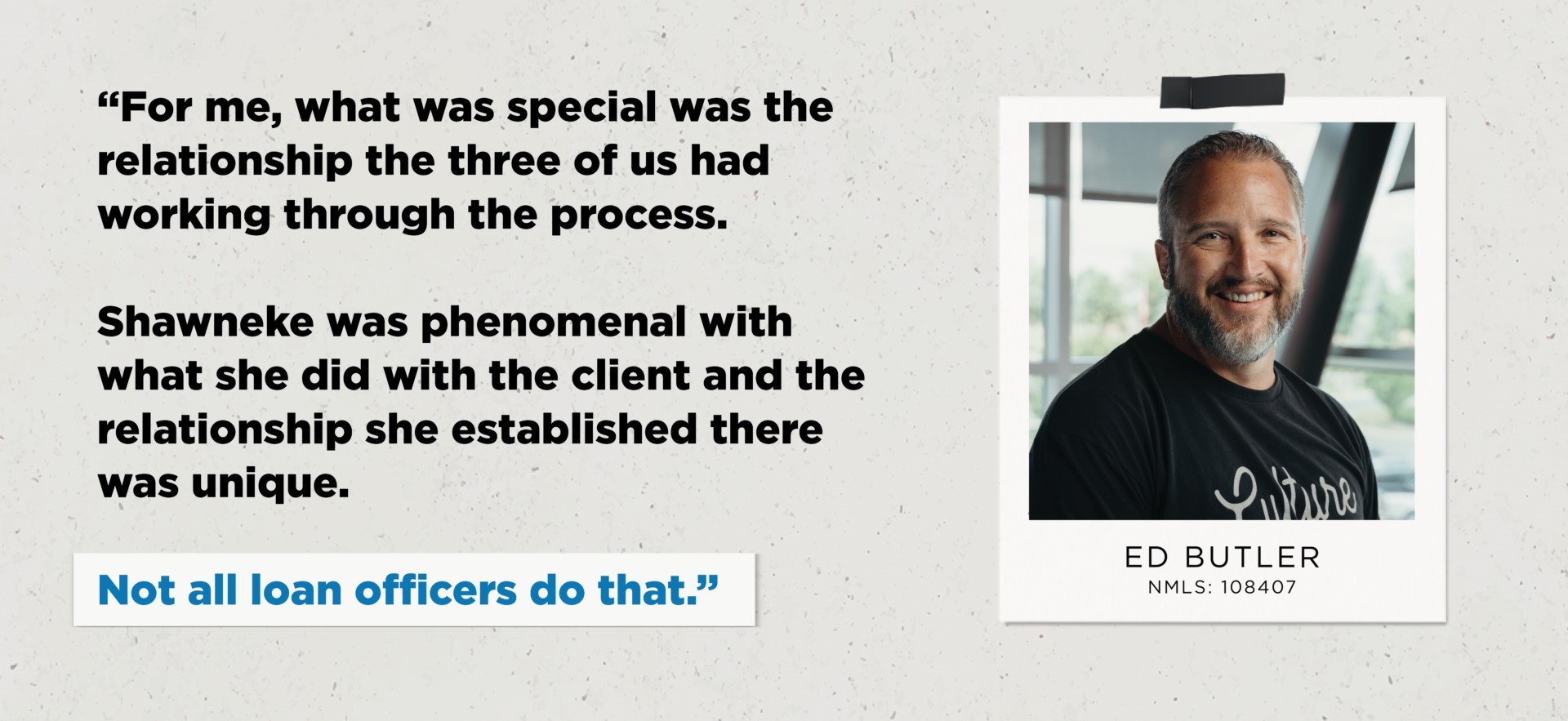

“For me, what was special was the relationship the three of us had working through the process,” Ed shares. “Shawneke was phenomenal with what she did with the client, and the relationship she established there was unique. Not all loan officers do that.”

Meaningful relationships are a testament to the culture at Movement Mortgage. “It was us coming back and forth with the buyer and working through it for her,” Ed says. “It's not the big bank mentality that this is just a transaction and you move on to the next one. 'You qualify for this but not that and good luck to you.' Instead, Shawneke worked with her for several months to get her where she could qualify and have a mortgage within her budget.”

Home sweet home

Teresa's home is a remodeled 1940's era, three-bedroom, two-bath home with walnut and pear trees in the yard. And it is within walking distance to her mother's house. It's the first mortgage Teresa has ever held in her name, and the monthly payment is just $10 more than what she was paying in rent. Teresa said her daughter is excited to have her own room, and together they have begun to decorate the house.

“The last minute before the closing was very emotional for me,” Teresa remembers. “It was emotional because it solidified that I was making the right decision, and this was my home. This was where I needed to be.”

“The most valuable part of the whole process was to know I had people that I created a bond with even after the closing,” Teresa says. “Shawneke will call me out of the blue to see how I'm doing. We shared a moment. We always say we are going to get together and have a cookout.”