How China’s currency led to a significant rate drop

Fear of a worldwide economic recession sent interest rates plummeting this week; the biggest move to the downside since Donald Trump was elected President. Only eight months ago the 10-year Treasury note traded at 3.25%. Earlier in the week the 10-year was trading at half of that with a low of 1.59% before heading higher Thursday as markets settled down a bit. Hopes for global growth are eroding especially after last week's federal funds rate cut by the Federal Reserve along with several other central banks easing around the globe this week.

The biggest fear is that the trade war between the United States and China will essentially halt global economies. Last week, President Trump announced additional tariffs on more Chinese exports. On Sunday, the People's Bank of China (PBOC) let its currency, the yuan, weaken to its lowest point in a decade. That provoked accusations from the U.S. that China was intentionally manipulating the value of the yuan as a tactic to hit back at tariffs.

Every evening, the PBOC sets the level at which the yuan will trade with the dollar. Where China sets its currency is extremely important because the weaker the currency, the less expensive Chinese goods are on the international market. Therefore making it easier for every other country to purchase Chinese goods that are heavily taxed in the U.S.

The Dow had its worst day of the year on Monday in reaction to China's weakening of the yuan, only to rebound Tuesday morning when the PBOC set the yuan at a stronger-than-expected level. This will be the thing to watch in the coming weeks as we approach Sept. 1, the date the new tariffs on Chinese goods will go into effect. Expect a lot of volatility until something meaningful gets done on the trade front.

Stocks edged out a little higher on Wednesday, despite a series of rate cuts from international central banks. Similar to the Fed's move last week, this is an effort to ease monetary policy to spur spending and hopefully, growth.

This week, New Zealand, India and Thailand all eased rates much more than was expected. New Zealand dropped its rates by 50 basis points, much higher than the predicted 25 bps. India made its fourth cut this year, dropping rates by 35 bps while Thailand made its first rate cut in four years, easing by 25 bps. Again, this sharp monetary action is all due to fears of a currency war, trade issues and associated weakening global growth expectations.

The producer price index data from July, just released Friday morning by the Labor Department, shows that there is potentially room for the Fed to ease the federal funds rate again next month. The PPI rose by 0.2% last month, with a year-over-year increase of 1.7%. That year-over-year number has remained flat which could open the door for a Fed rate decrease again next month. Plus, the core PPI, which excludes volatile costs, fell by 0.1%. That's the first dip in core PPI in nearly four years.

So how does that affect my mortgage rate?

When economies slow, especially when impacted by geopolitical concerns, U.S. Treasury bond prices go up and Treasury yields go down as investors seek the safety of government-backed bonds. Mortgage interest rates typically follow the trajectory of longer term Treasury yields such as the 10-year Treasury note.

Earlier this week, the yield on the 10-year Treasury note took a nosedive. On Aug. 1, the yield was trading at 2.05% and moved significantly lower with an intra-week low of 1.59%. This week, things settled down a little on Thursday as the stock market erased Monday's losses, with the 10-year Treasury note trading at 1.70%. You can see the steep decline in the chart below. The chart goes back three years, following the 10-year Treasury Note. That number is typically a very good indicator of the movement of long-term mortgage rates, like the 30-year fixed rate.

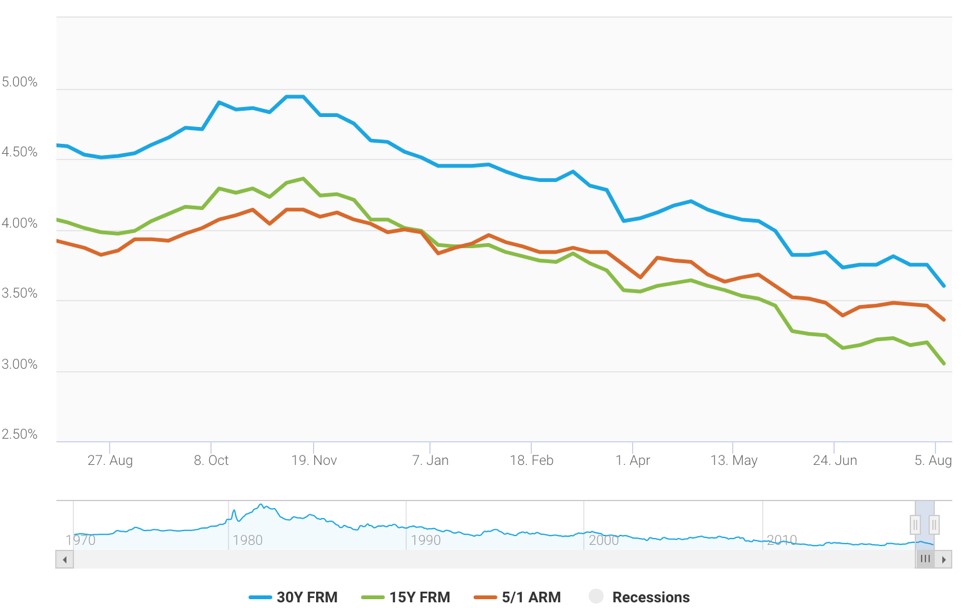

Thursday morning, the Freddie Mac average for the 30-year fixed-rate mortgage showed a significant week-over-week drop to 3.6%. It had been holding steady at 3.75% the last two weeks, and you can see in this chart from Freddie Mac just how much rates have fallen over the last year. The blue line shows the 30-year fixed-rate average and we were sitting at 4.59% August 2018.

According to the analysis from Freddie Mac, there is a tug of war happening between business and consumers. Business sentiment continues to be on the negative side because of trade and manufacturing problems while consumer sentiment is positive, bolstered by a strong labor market and very low interest rates.

Refinances should continue to drive the housing market, however, as the recent drop in rates means the number of people who would benefit from a refinance has gone up by 1.5 million, according to data from Black Knight. That data shows that there are a total of 9.7 million people who could cut their rate by 0.75%, saving them about $267 per month over the life of the mortgage. Let's say you have 15 years left on your mortgage. If you refinanced and lowered your rate by 0.75% right now, you'd save around $48,000 over the remaining life of the loan.

Inventory issues plague housing

Inventory continues to be a bugaboo for the housing market and it's a complicated issue. Chief economist for the National Association of Realtors, Lawrence Yun, points to the construction industry as half the battle. "New home construction is greatly needed; however, home construction fell in the first half of the year," Yun said. "This leads to continuing tight inventory conditions, especially at more affordable price points. Home prices are mildly reaccelerating as a result."

The median price for a home in the United States is now $279,600 according to data from the NAR. That's an increase of 4.3% annually in the second quarter. That, as Yun points out, is a result of lack of inventory. But it's not as simple as just saying home builders need to build more homes.

There is a big issue with labor shortages across the United States. The National Association of Home Builders actually marked labor shortages as their main challenge going forward in 2019. As of June of this year, the number of open construction jobs hit 404,000, it's highest level since the Great Recession. Coupled with the cost of production materials going up, the lack of workers available to build homes has put upward pressure on new home prices. That prices out many first-time homebuyers and leads to construction companies pulling back on building because it is not as cost-effective.

Also, as we mentioned two weeks ago, older Americans are staying in their homes longer, which is also a factor in decreasing supply. The study by First American showed that tenure length, meaning how long someone stays in their home, has increased by 0.7%. That contributed to a 33,000 reduction in new home sales.